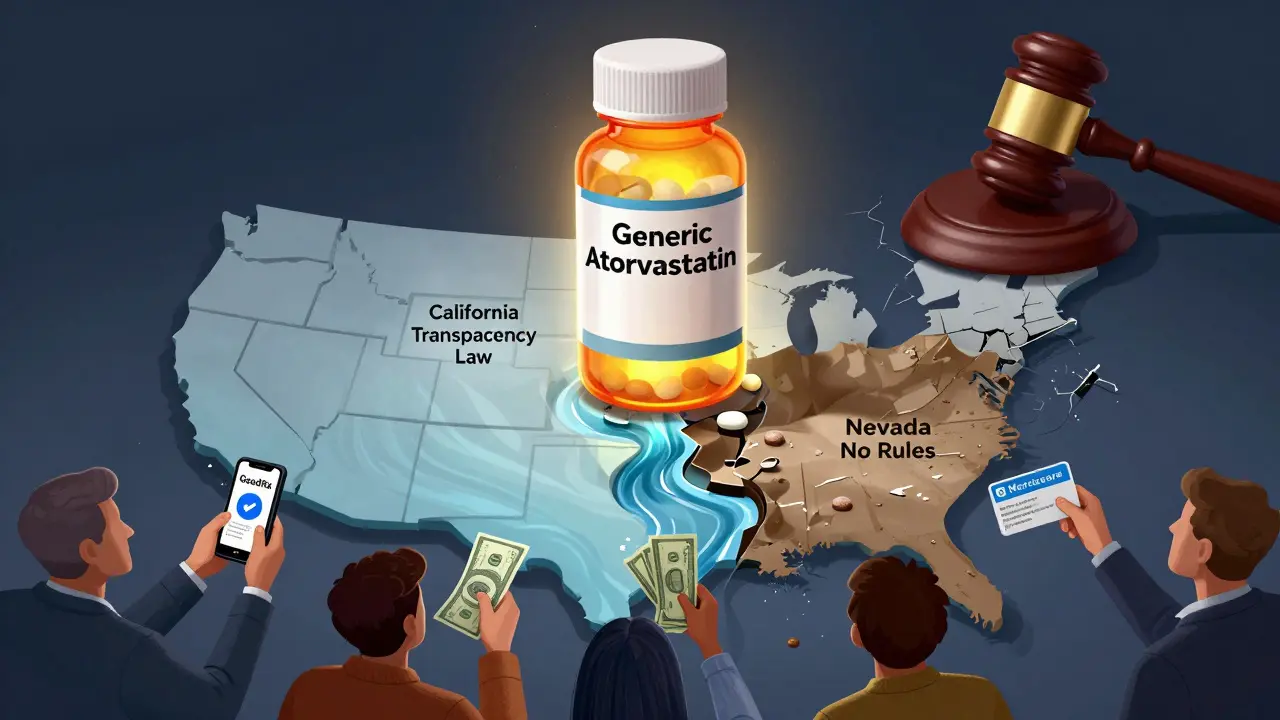

Have you ever filled a prescription for a generic drug and been shocked by the price - only to find out a friend in another state paid half as much for the exact same medicine? It’s not a mistake. It’s not a glitch. It’s the reality of how generic drug pricing works in the U.S. The same 30-day supply of generic atorvastatin can cost $12 in Ohio and $110 in Nevada. Why? Because state laws, pharmacy benefit managers, and market competition don’t work the same way everywhere.

How the Same Drug Costs Different Amounts Across States

Generic drugs are supposed to be cheap. They’re copies of brand-name pills, made after patents expire. By law, they must be chemically identical. So why do prices swing wildly? The answer lies in how each state handles reimbursement, contracts, and transparency.

Some states, like California and Vermont, passed laws forcing drug manufacturers and pharmacy benefit managers (PBMs) to report pricing data. These transparency rules mean pharmacies and insurers can’t hide markups. In states without these laws, PBMs - the middlemen who negotiate drug prices for insurers - often set prices behind closed doors. The result? Patients pay more, even if their insurance says they’re covered.

Take Medicaid, which covers 80 million Americans. Each state sets its own reimbursement rate for generic drugs. Some use the National Average Drug Acquisition Cost (NADAC), updated monthly. Others use older benchmarks or even negotiate rates directly with PBMs. In states that use NADAC, prices stay closer to wholesale cost. In states that don’t, prices can balloon.

The Role of Pharmacy Benefit Managers (PBMs)

PBMs are the hidden drivers of price variation. They’re not pharmacies. They’re not insurers. They’re contract negotiators who work for big health companies. They get rebates from drugmakers, charge pharmacies fees, and decide what patients pay at the counter.

Here’s the twist: PBMs often make more money when patients pay more. How? Through spread pricing. If a PBM agrees to pay a pharmacy $10 for a drug but charges the insurer $40, they pocket the $30 difference - unless state law bans it. States like Maryland and New York have cracked down. Others haven’t.

Research from the USC Schaeffer Center found that in states with weak PBM oversight, patients overpay for generics by 13% to 20%. That’s billions of dollars a year. And it’s not random - it’s tied to which state you live in.

Why Cash Often Beats Insurance for Generics

Here’s a counterintuitive truth: if you’re paying for a generic drug out of pocket, you might pay less than if you use insurance.

Why? Because insurance claims go through PBMs, who set inflated prices. But when you pay cash, pharmacies can use lower wholesale prices - especially if they’re independent or part of a discount network like GoodRx or Cost Plus Drug Company.

GoodRx data from 2022 showed that for the same generic drug, cash prices were 30% to 70% lower than insurance prices in many states. In rural areas, where pharmacy competition is low, the gap is even wider. A 90-day supply of generic metformin cost $15 in cash in Iowa but $120 with insurance in Alabama.

And it’s not just low-income people doing this. A 2020 study found that 4% of all generic prescriptions were paid in cash - but 97% of those cash payments were for generics. People figured it out. They’re avoiding insurance-driven markups.

State Laws That Changed the Game

Not all states sit back. Some took bold steps.

- Vermont (2016) - First state to require drug price transparency. Forced manufacturers to report price hikes.

- California (2017) - Created a public database of drug prices. Patients can compare costs before filling prescriptions.

- Maryland (2017) - Passed a law banning “price gouging” on generics. Got sued. A federal court struck it down, saying states can’t regulate interstate commerce.

- Nevada (2018) - Targeted diabetes drug prices. The lawsuit was dropped, likely to avoid legal exposure.

Even when states win, they lose. The Maryland ruling sent a chill through other states. Now, instead of capping prices, most states focus on disclosure. That helps - but it doesn’t stop markups.

The Impact of Medicare’s New Caps

The Inflation Reduction Act of 2022 brought big changes - but only for Medicare Part D users. Starting in 2025, insulin will cost no more than $35 a month. Out-of-pocket drug spending will be capped at $2,000 annually.

That’s huge - but it helps only 32% of drug users. The other 68% - people under 65, privately insured, or uninsured - still face wild price swings.

And here’s the catch: even Medicare beneficiaries don’t get the same prices everywhere. A 2023 CMS analysis found that in states with strong transparency laws, Medicare patients paid 8% to 12% less for generics than in states with weak oversight. The system is still fractured.

Why Rural Areas Pay More

It’s not just state lines - it’s county lines.

In rural areas, there’s often only one pharmacy. No competition. No pressure to lower prices. A 2022 study found that generic drug prices in rural counties were 22% higher on average than in urban areas, even within the same state.

Why? Because rural pharmacies don’t have the volume to negotiate better wholesale rates. They also can’t afford to join discount networks. So they charge what they need to stay open.

Patients in places like eastern Kentucky or western Nebraska often have to drive 50 miles to find a better price - or order online.

What You Can Do Right Now

You don’t need to wait for a law to change. You can take control today.

- Check GoodRx or SingleCare - Enter your drug, your zip code. See cash prices. Compare to your insurance copay.

- Ask for cash pricing - Even if you have insurance, ask the pharmacist: “What’s the cash price?” Sometimes it’s cheaper.

- Use mail-order pharmacies - Many offer 90-day supplies at lower rates. Especially useful if you’re on a stable medication.

- Know your state’s rules - If you live in California, Vermont, or New York, you have access to public pricing databases. Use them.

- Consider Cost Plus Drug Company - They sell generics at wholesale cost plus a flat $5 fee. No insurance needed. Available online nationwide.

One patient in Texas told me she switched from insurance to GoodRx for her generic lisinopril. Her monthly cost dropped from $67 to $9. That’s not luck. That’s knowing how the system works.

The Bigger Picture

Generic drugs make up 90% of prescriptions in the U.S. But they account for only 18% of total drug spending. That’s because prices are artificially high - not because of manufacturing costs, but because of how the system is structured.

Drugmakers don’t set these prices. PBMs do. States don’t have full power to fix it. And patients? They’re left to navigate a maze.

But change is coming. More states are creating drug affordability boards. More PBMs are being forced to disclose fees. More patients are learning to pay cash.

The system is broken - but it’s not hopeless. The price of your pill isn’t random. It’s a product of policy, power, and geography. And now, you know how to beat it.

Why do generic drug prices vary so much between states?

Generic drug prices vary because each state has different rules about how pharmacies and pharmacy benefit managers (PBMs) set prices. Some states require transparency and limit markups, while others let PBMs charge whatever they want. Medicaid reimbursement rates, pharmacy competition, and local market power all play a role. For example, California’s public pricing database helps keep costs lower, while states without such laws often have higher prices.

Is it better to pay cash or use insurance for generic drugs?

For many generic drugs, paying cash is cheaper - sometimes by 30% to 70%. That’s because insurance claims go through PBMs, who inflate prices to earn rebates and fees. Cash payments skip that system and let you access lower wholesale prices. Services like GoodRx or Cost Plus Drug Company show you exactly what you’d pay out of pocket. Always ask your pharmacist: "What’s the cash price?" before using insurance.

Do state laws actually lower generic drug prices?

Yes - but only in some states. States like California, Vermont, and New York have transparency laws that force drugmakers and PBMs to report prices. Patients in these states pay 8% to 12% less on average for generics than those in states without such laws. However, attempts to directly cap prices - like Maryland’s 2017 law - were struck down by federal courts. So while disclosure helps, direct price control is still legally risky for states.

Why are rural areas more expensive for generic drugs?

Rural areas often have only one or two pharmacies, which means little competition. Pharmacies there can’t negotiate lower wholesale prices because they don’t sell enough volume. They also rarely join discount networks like GoodRx. As a result, prices are 20% to 25% higher on average than in cities. Patients in rural regions often have to drive farther or order online to find better deals.

Will the Inflation Reduction Act fix state-level pricing differences?

Not directly. The Inflation Reduction Act’s $35 insulin cap and $2,000 annual out-of-pocket limit only apply to Medicare Part D users - about one-third of drug users. It doesn’t change how PBMs set prices for privately insured or uninsured people. However, it has pushed more attention to drug pricing overall, which may encourage more states to adopt transparency laws. But for now, state differences remain wide.